Overview

On June 1, 2018, the Trump Administration extended its Section 232 tariffs on imports of steel and aluminum to cover imports from Canada, Mexico, and the European Union (EU). The US had previously granted Section 232 tariff exemptions for these countries (and for Australia, Argentina, Brazil, and South Korea) and instead sought to negotiate quotas or alternative arrangements. As we explained in previous alerts, the Section 232 tariffs were imposed by the President after the US Department of Commerce (DOC) determined that imports of steel and aluminum threaten to impair US national security.

In announcing that Canadian, Mexican, and European steel and aluminum would become subject to the tariffs, Secretary Wilbur Ross stated that insufficient progress had been made in negotiations with the EU to warrant further extension of its exemption. Secretary Ross also stated that insufficient progress had been made in NAFTA renegotiations to warrant further exemption of Mexico and Canada. The United States reached quota agreements with Argentina, Brazil, and South Korea as an alternative to steel tariffs. Argentine aluminum is also now subject to a quota instead of tariffs, but Brazilian and South Korean aluminum is now subject to tariffs. Australian steel and aluminum remain exempt from both quotas and tariffs at this time.

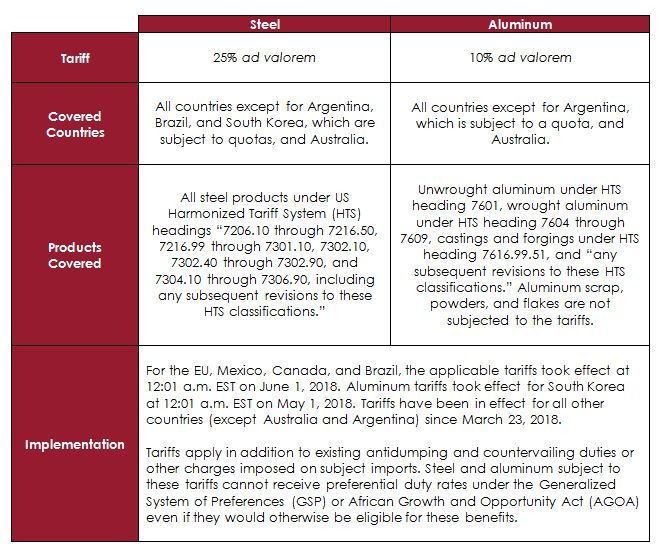

Certain steel imports from the EU, Mexico, and Canada that have entered the US since June 1 are thus now subject to 25% ad valorem tariffs, and certain aluminum imports from these countries (and from South Korea and Brazil) are now subject to 10% ad valorem tariffs (see Figure 1). In response, the EU, Canada, and Mexico have each announced plans to retaliate against US exports. In addition, Mexico and the EU challenged the Section 232 tariffs at the World Trade Organization (WTO), and Canada challenged the tariffs both at the WTO and via the NAFTA dispute settlement system.

Section 232 Tariffs as of June 1, 2018 (Figure 1)

The following table summarizes the coverage of the Section 232 steel and aluminum tariffs as of June 1, 2018:

Responses from the EU and NAFTA Countries

The EU, Mexico, and Canada have all taken steps to retaliate against US exports in response to the Section 232 tariffs.

When the Section 232 tariffs were first announced in March 2018, the EU released a proposed list of US products to target with potential retaliatory tariffs. That list included steel and aluminum, textiles and apparel, boats, glass products, and politically-sensitive US exports such as motorcycles, bourbon, corn, and other agricultural products.

On May 16, the EU published a notice in its Official Journal establishing retaliatory measures against US exports. According to this notice and an EU notification to the WTO, the EU will impose tariffs in two rounds on approximately $7 billion-worth of US exports. The first round will involve 25% tariffs on $3.2 billion-worth of US exports and, as announced by the European Commission on June 6, is expected to take effect in July 2018.

In the second round, the EU will impose tariffs at varying levels on another $3.8 billion-worth of US exports, either on March 23, 2021 or once a WTO panel rules against the Section 232 tariffs, whichever comes sooner. Together, the two rounds of planned EU retaliation will target a product list largely identical to the list published in March 2018.

Canada has also published a proposed list of US exports on which to impose retaliatory tariffs. Canada proposes to target $12.8 billion-worth of US exports of steel and aluminum products, consumer items, chemicals, and food products such as candy, preservatives, and condiments. The Canadian Government will accept comments from Canadian stakeholders on this list until June 15, 2018 and plans to impose tariffs on July 1, 2018.

On June 5, 2018, Mexico imposed tariffs ranging from 7% to 25% on US exports of steel and food products including pork products, cheeses, potatoes, bourbon, and apples. For certain pork and cheese products, tariff rates will increase from immediately effective levels of 10% or 15% to levels of 20% or 25% on July 5, 2018. Mexico also established a quota allowing for a total of 350,000 tons of pork from all sources, including from the US, to be imported tariff-free in 2018. (US pork exported to Mexico has been duty-free under NAFTA, but Mexico still maintains tariffs on pork from other countries. However, exports from any country including the US can count towards this new quota). The Mexican Economy Ministry has reportedly estimated that its retaliatory measures affect $3 billion-worth of US exports to Mexico. Both Mexico and Canada have stated that their retaliatory tariffs will remain in effect until the US removes its tariffs on their steel and aluminum exports.

Although the US Section 232 tariffs are now in effect and the EU and NAFTA countries have taken steps to retaliate, Secretary Ross had stated on May 31, 2018 — after announcing the end to the EU and NAFTA tariff exemptions — that the US remained “eager to have further discussions” with the EU and NAFTA countries.

Quotas as Alternatives to Tariffs for Argentina, Brazil, and South Korea

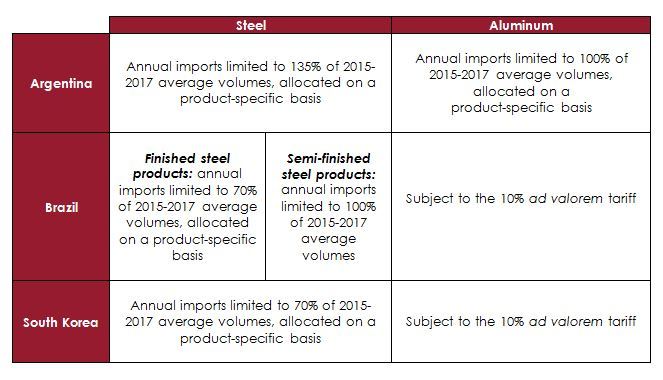

US imports of South Korean steel, Brazilian steel, and Argentine steel and aluminum remain exempt from the Section 232 tariffs but are instead now subject to annual quotas covering imports that have entered the US since January 1, 2018.

For Argentina and Brazil, these quotas became effective on June 1, 2018. The quota for South Korea became effective on May 1, 2018 after the US and South Korea finalized an agreement to limit South Korean steel imports. As part of that agreement — which also includes amendments to the US-Korea Free Trade Agreement (KORUS) and Korean regulatory and trade policy changes in line with KORUS — annual US imports of South Korean steel products are limited to 70% of the average of 2015-2017 volumes, allocated on a product-specific basis. For 2018 (and onward), these quotas apply to imports for the full calendar year and therefore were already partially filled when announced.

The following table summarizes the import restrictions on steel and aluminum from Argentina, Brazil, and South Korea (Figure 2):

The quotas established for Brazilian and Argentine steel also apply to imports for entire calendar years (including 2018) and are allocated at the same product-specific levels at which the South Korean steel quota is divided. The Argentine aluminum quota applies to full calendar years including 2018 as well and is allocated between unwrought and wrought aluminum (see Figure 1 for a description of these categories).

According to the June 1, 2018 Presidential Proclamations concerning steel and aluminum, countries subject to annual quotas will also be subject to quarterly limitations. Starting on July 1, 2018, a subject country’s exports of a particular steel or aluminum product cannot exceed “500,000 kg and 30%” of the annual product-specific quota in a given quarter.

Like imports subject to the Section 232 tariffs, imports subject to these quotas are not eligible for Generalized System of Preferences (GSP) duty-free treatment even if they otherwise would be. This will likely have a greater impact on aluminum than steel, since various aluminum imports are subject to other tariffs while steel imports are typically duty-free already (aside from antidumping and countervailing duties in place).

These are hard quotas, and imports cannot exceed the quota limit even with the duties imposed. In addition, the DOC will reportedly not consider exclusion requests pertaining to products imported from countries subject to quotas (i.e. only requests for the exclusion of specific products subject to tariffs will be considered). Still, according to the June 1, 2018 Presidential Proclamations, the Secretary of Commerce is directed to “inform the President of any circumstance that in the Secretary's opinion might indicate that an adjustment of the [quotas] is necessary” and the President has the authority to adjust quota levels in the future.

Section 232 Exemption for Australia

Australia will continue to remain exempt from tariffs at this time as the US stated that they have reached an arrangement allowing Australia to remain exempt from the Section 232 measures. However, further details of the deal remain unknown and no quotas have been implemented.

According to the Presidential Proclamations, any of the countries not subject to the tariffs (including those subject to quotas) may have also agreed with the US on measures to reduce excess global steel and aluminum production and capacity, support the US industries, prevent US import surges, and prevent transshipment of subject steel and aluminum through exempted countries.

Next Steps for Concerned Companies

Concerned companies should assess their exposure to the updated US restrictions on steel and aluminum as well as the European, Canadian, and Mexican retaliatory measures. Companies should also assess how the removal of GSP-eligibility for steel and aluminum imports subject to tariffs or quotas might affect their business.

As is evident from US, European, Canadian, and Mexican governments’ statements and actions, there may be additional, significant changes to the terms of trade between the US and its North American and European allies in the coming months. Companies would be wise to remain abreast of developments in US-EU and NAFTA trade discussions to understand how they may be affected.