Overview

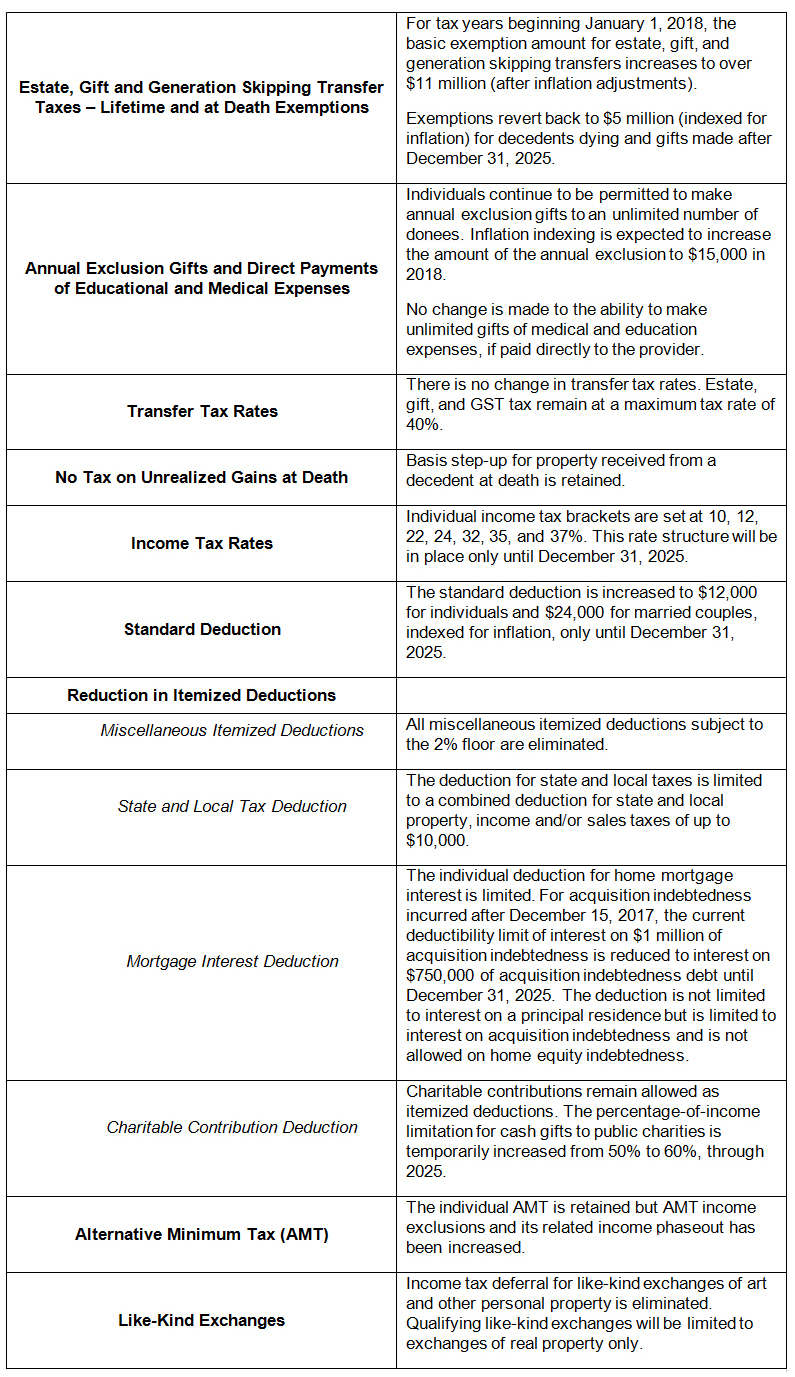

Congress has passed sweeping tax legislation affecting the taxation of corporations, businesses, insurance companies and banks, compensation and retirement savings, exempt organizations, and individuals, which will become law when the bill is ultimately signed by the president. Of particular relevance to our clients are the increase in the estate, gift and generation skipping transfer (GST) tax exemptions, changes to the individual income tax rates, and the elimination of most individual income tax itemized deductions.

As 2017 comes to a close, Steptoe’s Private Client practice would like to take this opportunity to highlight some of the provisions affecting individuals, as well as certain year-end planning opportunities.

2017 Year End and Immediate Considerations

- Annual gifts of up to $14,000 per person may be made to an unlimited number of individuals without consuming any lifetime exemption amount or incurring a gift tax. A married couple together is able to gift $28,000 to each donee in 2017. The limitation on annual gifts made to a noncitizen spouse is capped at $149,000 in 2017.

- Federal estate, gift, and GST tax exemption amounts may be used to make gifts during lifetime or at death. The amount is currently capped at $5.49 million for 2017. We do not recommend making gifts beyond this amount and incurring gift tax, as starting January 1, 2018 those exemption amounts are nearly doubled.

- Consult with your accountant to determine whether bonuses and other income should be accelerated to 2017 or deferred until 2018 (if possible). Decisions will have to be made taking into account how the reduction in tax rates offsets the loss of state and local income tax deductions in 2018.

- Determine with your accountant whether you will realize a tax advantage by paying any estimated state income taxes on 2017 income prior to December 31 (rather than waiting until January 15) in order to take a 2017 deduction for the state income tax paid.

- Consider making charitable gifts in 2017 if you are unlikely to itemize deductions in 2018 as a result of the tax law changes.

- Maximize annual IRA and other deferred compensation contributions.

- Review current estate plans to ensure any formula gifts are still appropriate, given the increased exemption amounts applicable in 2018.

- Make sure all necessary “Crummey Notices” have been sent to appropriate parties to ensure corresponding gifts made in trust qualify for the annual exclusion (particularly applicable to insurance trusts).

Things to Consider Going Forward Into 2018

- Consider making additional gifts to take advantage of the limited window of time for increased gift tax exemption planning. Gifts made during your lifetime remove both the value of the gifted property as well as any appreciation on that property from your taxable estate, thus minimizing what may be taxed at your death. The basic lifetime exclusion amount doubles as of January 1, 2018 to $10 million and after inflation adjustments will be over $11 million. This allows for a significant amount of additional lifetime gifting without gift tax consequences.

- Property included in your taxable estate will continue to receive a step-up in basis at your death. Assets gifted during your lifetime will not receive a step-up in basis at death. Therefore, income tax considerations must be taken into account in deciding whether to make lifetime gifts. For those whose total taxable estate is well under the new higher exemption levels it may make sense to consider “undoing” certain plans to bring appreciated assets back into the estate. However, the avoidance of capital gain tax must be weighed against any consequent state level estate taxes on such assets as well as the risk that the assets will appreciate beyond the exemption actually available at the time of death.

- State transfer tax laws must also be taken into consideration. For example, although New York raised its estate tax exemption to eventually match the federal exemption, the increase was being phased in over several years and would not fully match the federal exemption until 2019. With the increased federal exemption, there will continue to be a disconnect between the New York and the federal exemption levels until 2026, when the federal exemption is slated to revert back to $5 million (indexed for inflation). In addition, the New York exemption is eliminated entirely for those estates that exceed the exemption amount by more than five percent. New York also includes certain lifetime gifts made between April 1, 2014 and January 1, 2019 and within three years of death in the decedent’s New York taxable estate.

- As interest rates are still low, but are likely to continue to increase, make intra-family loans.

- Review your current estate plan to ensure that it appropriately addresses major life events such as a marriage, divorce, or birth of a child or grandchild.

- Consider whether existing trusts need to be decanted to adjust the way property is distributed to certain beneficiaries by changing the trust provisions.

- Review all beneficiary designations to ensure that they do not conflict with your overall testamentary plan.

- Lifetime gifts may be further leveraged by the use of dynasty trusts to which GST tax exemption is allocated. These transfers allow property to pass in trust for the benefit of multiple generations free of estate, gift, and GST tax. Dynasty trusts also are an extremely valuable tool to protect assets from creditors, including spouses in the event of a divorce, to make sure younger generations are protected from having too much wealth in their own hands, and in some cases to preserve unity of ownership.

Grantor Retained Annuity Trusts (GRATs) and Sales to Grantor Trusts (GTs)

Low interest rates continue to make GRATs and sales to grantor trusts attractive and effective planning tools.

- Sales to GTs

- Sales to GTs using loans continue to be especially useful as proposed regulations under Section 2704 of the Internal Revenue Code, which would have limited the utility of sales of discounted family business interests to GTs, have been withdrawn.

- With increased gift exemption amounts, notes previously issued in sales to GTs may be forgiven.

- How sales to GTs work:

- The grantor of a GT is treated as the owner of the trust assets for income, but not estate tax, purposes. Thus, a grantor may sell assets that are likely to appreciate to a GT in exchange for a reasonable down-payment and a promissory note bearing a minimum required interest rate for the balance. No taxable gain is recognized on the sale and no interest income is recognized by the grantor because the trust is a GT for income tax purposes. So long as the trust assets appreciate by more than the applicable interest rate charged on the note (currently 1.52% for short term loans or 2.64% for long term loans entered into in December 2017), the appreciation over the applicable interest rate on the purchased assets will pass free of estate and gift tax.

- The grantor pays the income tax liability on the GT assets, which allows the principal to grow undiminished by the payment of income taxes. Because the grantor is the owner of the assets for income tax purposes, the grantor’s payment of the GT’s income taxes is not treated as a gift to the trust beneficiaries even though it results in an increased amount of trust assets available for distribution.

- GRATs

- A GRAT requires that the grantor retain a fixed annual annuity from the trust for a term of years.

- The annuity retained may be equal to 100% of the amount used to fund the GRAT, plus the IRS assumed rate of return applicable to GRATs. As long as the GRAT assets outperform the IRS assumed rate of return applicable to GRATs (currently 2.6% for December 2017), at the end of the annuity term the grantor will be able to achieve a transfer tax-free gift of excess appreciation on those assets. Under current law the grantor may structure a GRAT so that no taxable gift is made. Therefore, if the grantor survives the annuity term, the appreciation on those assets will pass outside of the grantor’s estate without using any applicable exclusion amount or incurring any gift tax.