Overview

Overview

The New York State Legislature approved the New York City (NYC) pied-à-terre tax on May 27, 2026, as part of the 2026-2027 state budget. The tax takes effect for NYC fiscal years beginning July 1, 2026, and applies to luxury second homes where the owner’s primary residence is outside New York City. The new law expires on June 30, 2031, unless renewed.

The tax was originally proposed by New York Governor Kathy Hochul on April 15, 2026, to support NYC Mayor Zohran Mamdani’s efforts to close NYC’s budget gap. The tax is aimed at luxury second homes in NYC and is expected to generate at least $500 million a year in recurring revenue for the city and to affect roughly 10,000 single family homes, co-ops, and condominiums citywide.

Application of the Tax

The pied-à-terre tax is an annual surcharge on residential properties over a certain value in NYC that are not occupied as a "primary residence" by a "covered owner."

Properties that meet one of the following tests will be exempt from the tax:

- The property is the primary residence of at least one covered owner.

- The property is the primary residence of an immediate family member of at least one covered owner.

- The property is leased out as rental units to a NYC primary resident and subject to a bona fide and negotiated arm’s length lease for a period of at least one year.

A "primary residence" is defined as a property that is the primary residence of the covered owner or "an immediate family member" of the covered owner (which includes a spouse, child, sibling, parent, grandparent, or grandchild). Whether a property qualifies as a “primary residence” is a factual determination and depends on how the property is being used. The residency status is measured as of January 5, immediately preceding the relevant fiscal year.

A "covered owner" includes:

- The individual owner of the covered property;

- In the case of a trust that owns the covered property, the "beneficial owners" who are the beneficiaries of the trust (but it is unclear how the law will apply where a trust has multiple discretionary beneficiaries); and

- In the case of a covered property owned by a corporation, partnership, or LLC, the shareholders, partners, or members holding a majority interest in such entity.

The law gives the New York City Department of Finance (NYC DOF) broad administrative discretion to determine if the property qualifies as a primary residence. The statute is vague and provides a determination will be made on factors identified by the NYC DOF including, but not limited to, whether the property was occupied in aggregate for a majority of days during the calendar year. Owners may be required to provide certification and documentation to prove the property was used as a primary residence. Penalties of up to 50% may be applied if the NYC DOF determines that the documentation submitted was inaccurate, misleading in a material way, or was submitted negligently or in bad faith.

Property owners determined to be subject to the tax will be notified by August 30, 2026. They will then have an opportunity to contest their inclusion.

Calculating the Tax

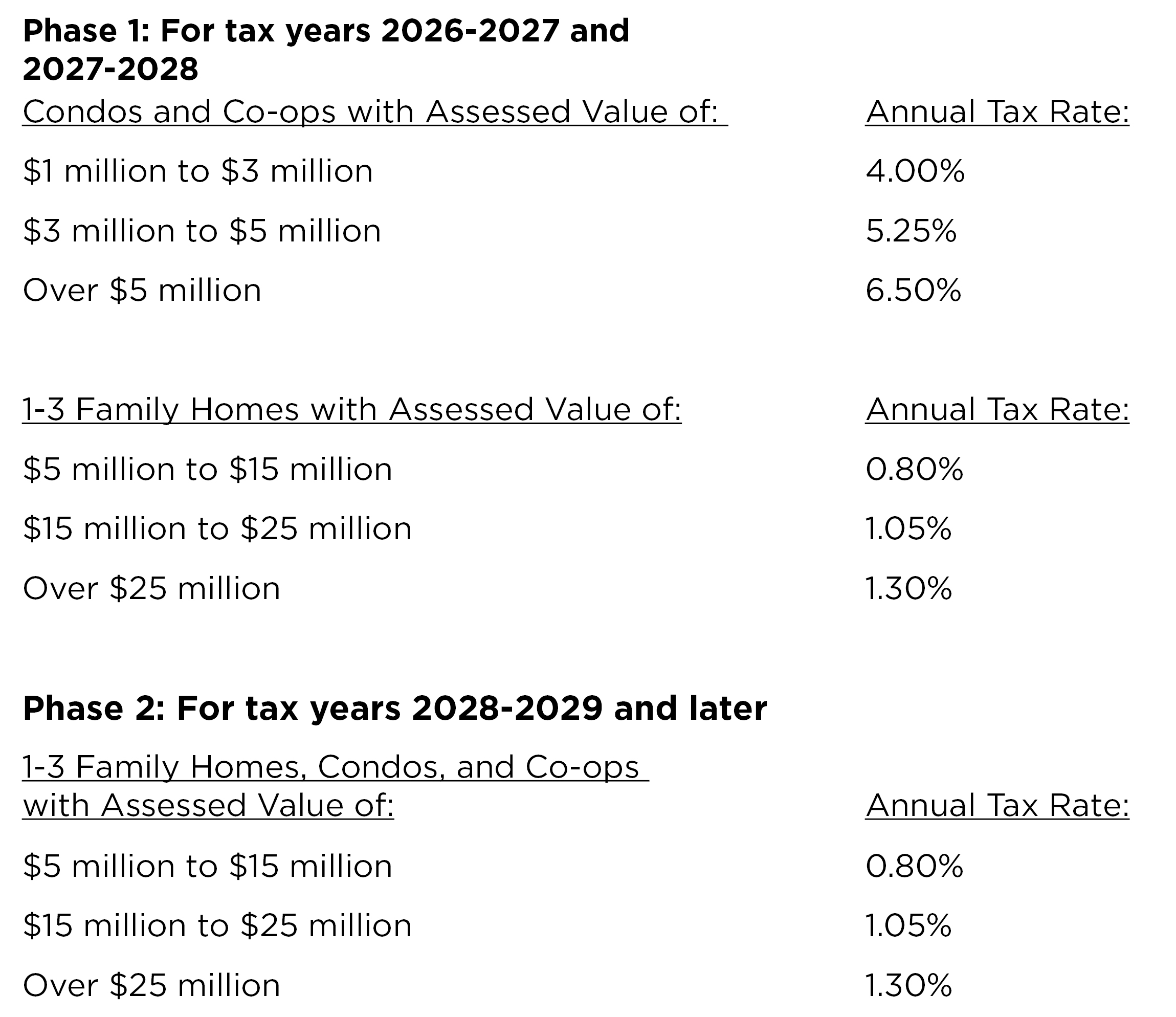

The calculation of the pied-à-terre tax piggybacks on the city's current residential property tax system which is imposed based on assessed values determined by the NYC DOF. Assessed values for co-ops and condominiums are determined based on hypothetical income and because of that have been historically lower than actual market value. Assessed values for other residential properties however are determined based on comparable sales data and are therefore more aligned with actual arm’s length transaction market values. Therefore, the tax will be imposed in two phases while the NYC DOF develops a new assessed value system for co-ops and condominiums also based on comparable sales prices.

Phase 1, beginning July 1, 2026, will apply the tax to one to three family homes with assessed values of $5 million or more and residential co-ops and condominiums with assessed values of $1 million or more. Phase 2, beginning July 1, 2028, will apply the tax to single-family homes, co-ops, and condominiums worth $5 million or more, as determined under the new assessed value system. In each phase, the tax will be imposed pursuant to the following tier structures:

What Is Still to Come

Beginning in the 2026-2027 tax year, the surcharge will be levied alongside real property taxes and enforced through similar collection mechanisms, including liens and foreclosure proceedings. The NYC DOF will have audit authority extending up to six years with regard to documentation submitted under the new law.

The two-phase rollout and accompanying updates to the city's assessment and valuation system to address properties it deems to be undervalued is extremely complicated. The details of how the NYC DOF plans to capture the value of residential co-ops and condominiums during the two-year transition phase have not yet been revealed. While the basic framework of the new law has been disclosed, important details in the implementation of the law, including the treatment of LLC and trust-owned residences, remain to be seen and challenges to the new law are likely. In particular, individuals who own properties through LLCs, trusts, or other entities should review their current ownership structures, operating agreements, and reporting practices to make certain they adequately address potential exposure to the new law.