Overview

Key committees in the Senate and House have concluded initial hearings on the Foreign Investment Risk Review Modernization Act of 2017 (FIRRMA), the CFIUS reform bill introduced in the Senate and House by Senator Cornyn and Representative Pittenger with bipartisan cosponsors on November 9, 2017. CFIUS, the Committee on Foreign Investment in the United States, is the interagency US government body originally created by President Ford in 1975 to review the national security implications of foreign investment activity in the United States. CFIUS reviews foreign acquisitions, mergers, and takeovers of existing businesses in the United States for US national security concerns.

This advisory identifies the main problems with the existing CFIUS process that have led to calls for reform, the mechanisms that FIRRMA would create to address those problems, and some of the key criticisms of FIRRMA that have been registered by congressional witnesses and others thus far.

Substantive Expansion of CFIUS Jurisdiction

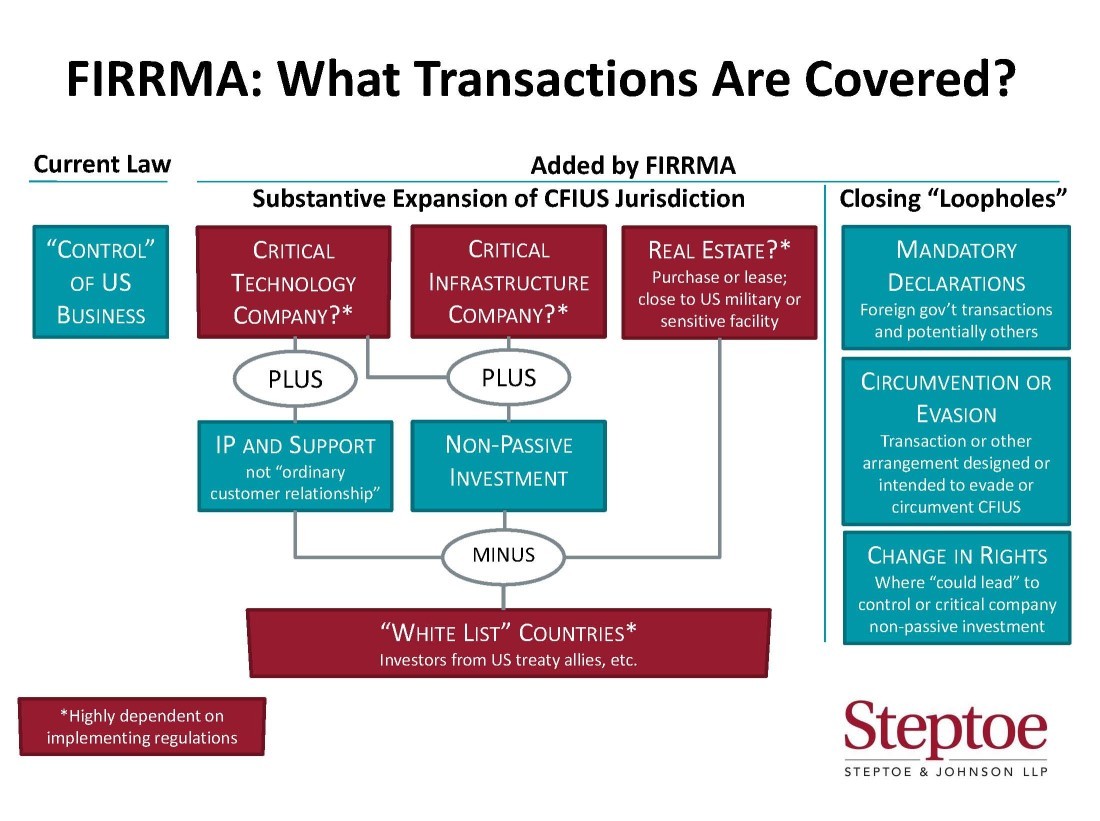

As explained in the attached chart (FIRRMA: What Transactions Are Covered?), FIRRMA would create several new categories of transactions that would be subject to CFIUS’s jurisdiction. Under current law, CFIUS’s jurisdiction is triggered only when a foreign investor acquires “control” over a US business. Critics of CFIUS suggest that some transactions – particularly in the high-tech sector – do not result in foreign “control,” but nonetheless should be subject to CFIUS review because of the type of technology that may be shared with the foreign person, or because of other national security sensitivities.

New categories of deals subject to CFIUS review: To address this and others concerns, FIRRMA would extend CFIUS to cover three new substantive categories of transactions:

- First, and most significantly, for US “critical technology” companies, CFIUS review would be required for transfers of “intellectual property and associated support” to a foreign person through a joint venture or any other arrangement other than an “ordinary customer relationship.”

- Second, for both US “critical technology” and “critical infrastructure” companies, CFIUS review would be required for “non-passive” investments of any type. “Passive” investments not subject to CFIUS review would mean no access to non-public technical information, no access to financial data not available to other shareholders, no board or other advisory positions, and no substantive decision-making role for the investor.

- Third, CFIUS review would be required for the purchase or lease of real estate in proximity to military installations or other facilities that have US national security sensitivities.

FIRRMA would provide the Department of the Treasury (Treasury) with substantial regulatory authority to modify the scope and application of these three categories by defining “critical technology,” and by further describing the types of critical infrastructure and real estate transactions that would trigger CFIUS review.

Most criticisms of the proposed expansion of CFIUS’s jurisdiction have focused on the first new category, which would authorize CFIUS review of any transfers of “intellectual property and associated support” by a critical technology company. A witness from IBM stated that this proposed change is a “serious flaw in the bill” that is “a principal reason the bill is controversial in the business community,” and predicted that it would result in CFIUS review of “many thousands of non-sensitive IP and technology licensing transactions.” Other witnesses described this change as unnecessary in light of the existing US export control regime, which already broadly regulates US technology exports.

On the other hand, Senator Cornyn and other proponents of the new “intellectual property and associated support” category justify it as necessary, particularly to address emerging technologies that are not easily susceptible to regulation through export controls. Proponents also note that FIRRMA would allow Treasury to exempt subcategories of transactions from review upon a finding that other provisions of law are adequate to address any national security concerns. We expect a continued, vigorous debate on the merits of using preexisting regulatory tools to address technology transfer versus creating new authorities to do so under CFIUS.

Exception for investors from “white list” countries: Several of FIRRMA’s sponsors and other critics of the current CFIUS process make no secret of the fact that they view China and its foreign investment strategy as one of the largest national security challenges to foreign investments in the United States. For example, Senator Cornyn indicated that “the context for [FIRRMA] is important and relatively straightforward, and it’s China.”

FIRRMA does not explicitly impose additional requirements on China or any other named country. However, it would give CFIUS the authority to create a “white list” of countries whose investors could be exempted from CFIUS review for the three new categories of transactions identified above. FIRRMA indicates that decisions related to placement on the “white list” should include considerations related to treaty alliances and the relevant country’s laws for screening foreign investments. Treasury would have significant discretion in deciding how to design the list.

While there appears to be broad consensus that CFIUS reform legislation should not explicitly call out problematic countries by name, some critics have suggested that authorizing the executive branch to create a “black list” would be a more effective and efficient approach. Under this approach, any new categories of transactions subject to CFIUS review would apply only to investors from countries that have been found by US national security agencies to be particularly problematic for US foreign direct investment from a national security perspective. Defenders of the bill as drafted point out that creating a black list could create serious diplomatic difficulties that a white list largely avoids. Moreover, FIRRMA does include a number of provisions that would encourage increased vigilance over transactions from “countries of special concern,” without identifying any such countries by name. We expect debate on country-specific mechanisms to continue over the coming months.

Closing CFIUS “Loopholes”

As a technical matter, the current CFIUS review process is voluntary. Companies choose to seek CFIUS’s preapproval of covered transactions because of the significant economic downside to an after-the-fact CFIUS review that may result in mandated changes to a transaction. In addition, under current rules companies have the discretion to construct transactions in a manner that avoids foreign control (and, thus, CFIUS jurisdiction). Some critics of CFIUS have characterized these features of CFIUS as “loopholes” that allow for evasion of the Committee’s review.

FIRRMA would address these perceived loopholes in a number of ways:

- For the first time, FIRRMA would mandate that parties to certain categories of covered transactions (including where a foreign government-owned entity would acquire a 25% or greater share in a US business) file with CFIUS. Parties would have the option to conduct these filings through an abbreviated “declaration” process or through submission of a typical written notice. (FIRRMA would also give parties to other covered transactions the option to file with CFIUS through the same declaration process).

- FIRRMA would also formally extend CFIUS jurisdiction to transactions “intended or designed to evade or circumvent” the CFIUS review process.

- CFIUS jurisdiction would also be extended to any transaction involving “any change in the rights” of a foreign person in a US business that could result in foreign control of a US business or a non-passive investment in a critical technology or critical infrastructure business.

Other Notable Aspects of FIRRMA

CFIUS resource needs: Data and anecdotal evidence indicate a significant increase in CFIUS filings in 2017, bringing filings to an all-time high. Simultaneous with this filing increase (and perhaps as a result of this increase) repeat participants in the CFIUS process have reportedly observed delays in the CFIUS process that harm investment prospects. In addition, some of the key CFIUS agencies have gone for months without political appointees in key senior-level positions with CFIUS responsibilities. Representative Kildee referred to “an underfunded and understaffed US government” as the second greatest threat, behind China, to US national security with respect to foreign investment.

Senator Cornyn and others have acknowledged that FIRRMA would increase CFIUS’s workload, and that CFIUS needs additional resources. Senator Cornyn testified that “for the price of a single B-21 bomber, we can fund an updated CFIUS process and protect our key capabilities for several years.” FIRRMA also includes a number of provisions designed to make it easier for CFIUS to maintain resources, from a new authority for CFIUS to fund its work through filing fees, to clear authorization for appropriations and a unified US government-wide CFIUS budget request, to specialized hiring authorities.

FIRRMA would not change the “national security” focus of CFIUS: A number of other countries with foreign investment review procedures do not limit their review to national security concerns. For example, Canada’s foreign direct investment review process under the Investment Canada Act is governed by a variety of (primarily) economic factors related to whether the investment “is likely to be of net benefit to Canada.”

FIRRMA retains national security as CFIUS’s only mandate. However, it does identify a number of additional factors for CFIUS to consider in conducting its national security analysis, including some that may seem relatively far afield of traditional national security decision making. For example, one new factor to be considered under FIRRMA would be the extent to which the transaction would expose “personally identifiable information, genetic information, or other sensitive data of United States citizens to a foreign government or foreign person that may exploit that information in a manner that threatens national security.”

Next Steps

FIRRMA represents a serious, bipartisan attempt to address shortcomings in the current CFIUS review process, and it has been endorsed by the White House as well as Secretary Mnuchin and other key senior officials in the Trump Administration. However, as summarized above, it is not without its critics. On Capitol Hill, some, including Senator Crapo, have expressed concern that any reforms to CFIUS should not deter from longstanding US policy of maintaining a free, fair, and open foreign direct investment climate. Others, including Senator Schumer, have called for additional review through a CFIUS-like process to consider whether foreign direct investments are economically harmful to the United States. We expect continued additional deliberations in Congress on CFIUS reform in the coming months.

We will continue to keep you informed of CFIUS developments. If you have any questions, please contact Stewart Baker at +1 202 429 6402, Brian Egan at +1 202 429 8009 or Alan Cohn at +1 202 429 6283 in our Washington office. Further commentary is available on the Steptoe International Compliance Blog. You can also follow us on Twitter (@SteptoeIntlReg).